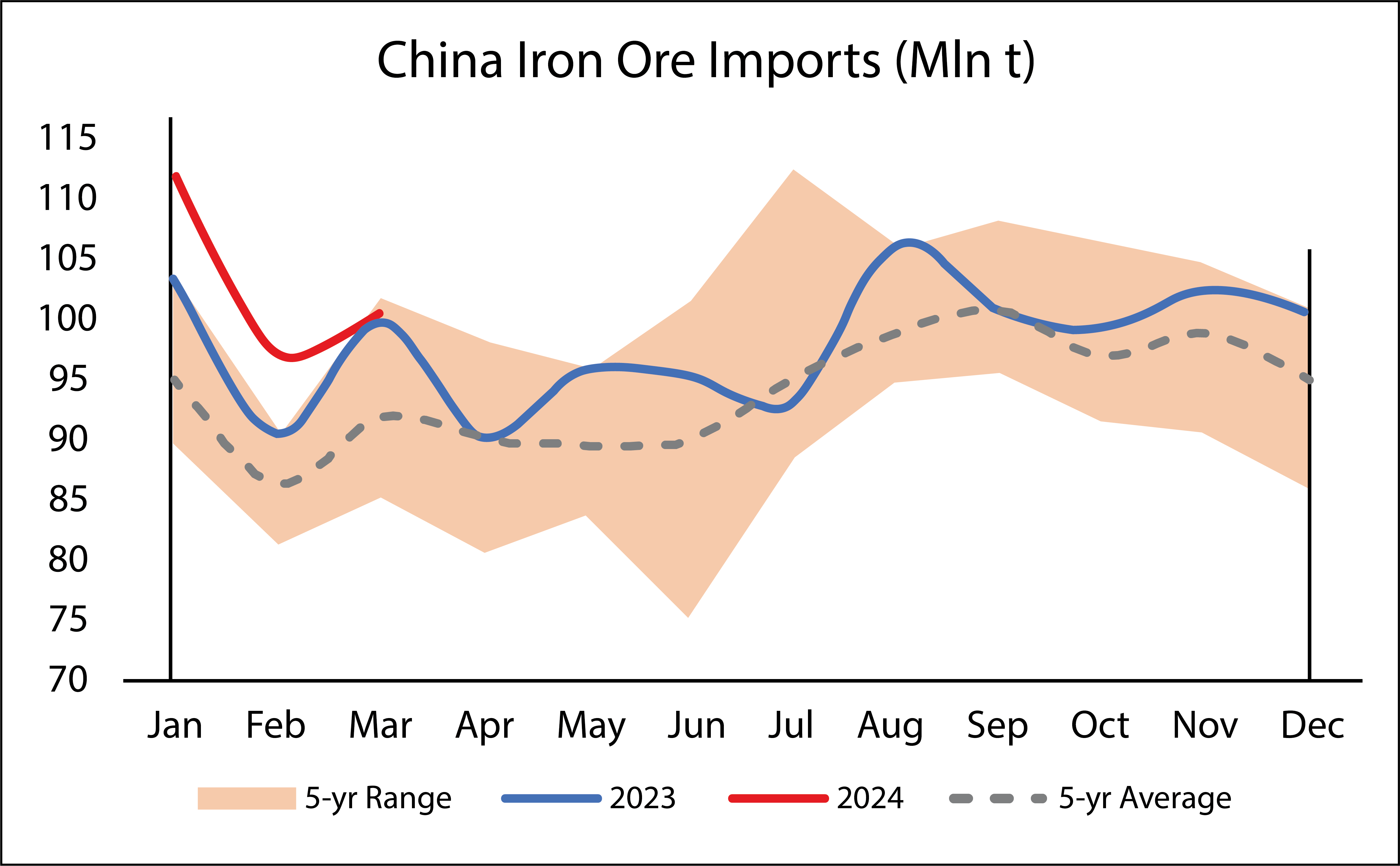

China’s iron ore imports witnessed a strong start in January and February, but imports in March 2024 were nearly flat year-on-year. The early months of January and February saw elevated iron ore prices, which could have influenced purchases during those months. Arrivals of those purchases were likely reflected in March due to the time lag between purchase and delivery.

Despite lowered prices since March, China’s iron ore market however still faces hurdles due to rising iron ore port inventories, a dwindling Steel PMI and continually soft property sector indicators. On the bright side, the relatively softer prices could provide opportunities for steel mills to build larger stockpiles during this period. A surprisingly strong Q1 GDP result could also cushion negative sentiments, and strong finished steel exports, particularly to Southeast Asia, could aid the steel market this year.